A narrative essay by Prabhjot S Bhatia

The headlines came fast and loud.

“India’s $5.4 Billion Shipbuilding Gambit Takes Aim at China—and Rattles the West.”

It’s the kind of framing that makes for a gripping geopolitical drama. But anyone who has lived inside shipyards, steel shops, design offices, and classification corridors knows: shipbuilding does not move at the speed of headlines. It moves at the speed of industrial memory, policy patience, and generational investment.

And India’s shipbuilding story is not a confrontation. It is an awakening.

A COUNTRY CATCHING UP WITH ITS OWN POTENTIAL

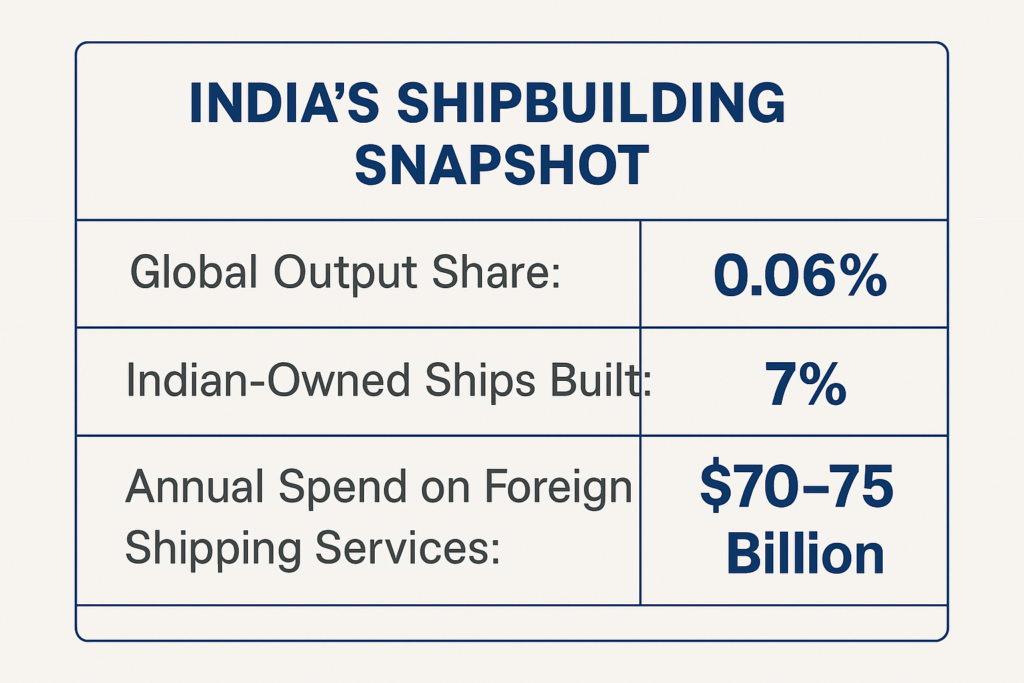

For decades, India outsourced its maritime backbone. Only 0.06% of global shipbuilding output comes from Indian yards. Just 7% of Indian-owned vessels were built at home. Every year, India pays $70–75 billion to foreign shipping services.

These numbers don’t point to rivalry. They point to a long, quiet neglect.

India is not trying to catch China. India is trying to catch itself — the version of itself that should have existed 30 years ago.

This is not a gambit. It is a correction.

THE MYTH OF THE INDIA–CHINA SHIPBUILDING RIVALRY

China’s shipbuilding dominance is not an accident. It is the result of:

- decades of consistent policy

- deep maritime financing ecosystems

- integrated supply chains

- massive economies of scale

- a national maritime consciousness

India is at the beginning of that journey. China is at the peak of it.

To suggest that India’s early steps “rattle” China is like saying a sapling threatens a forest.

China is not threatened. If anything, China stands to benefit.

A MORE CONSTRUCTIVE LENS: INDIA–CHINA SYNERGY

Shipbuilding does not grow through confrontation. It grows through regional clusters.

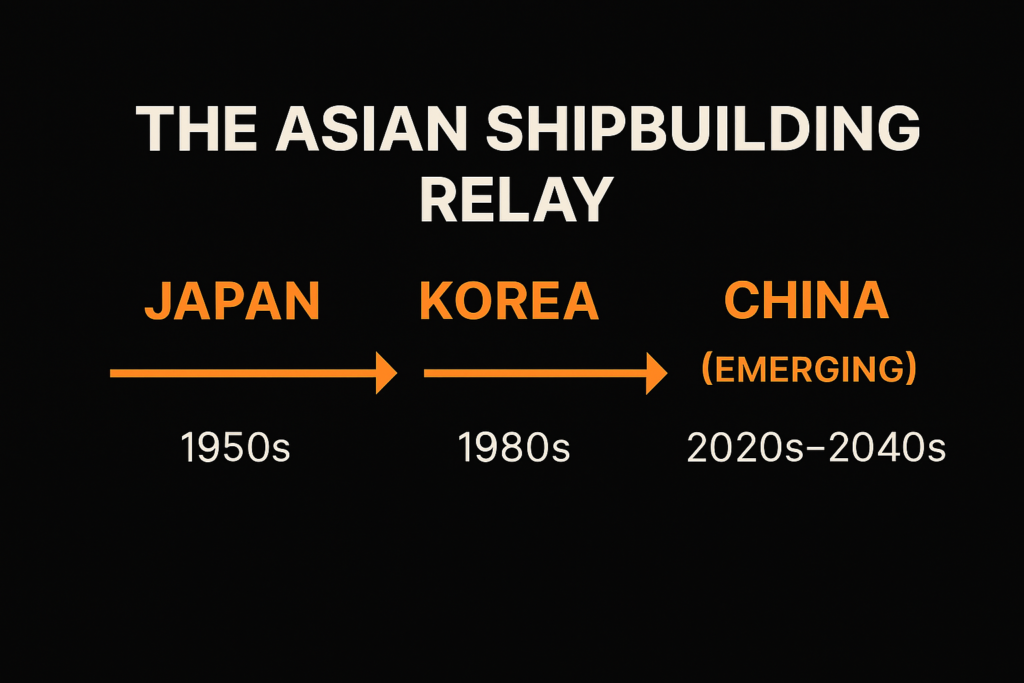

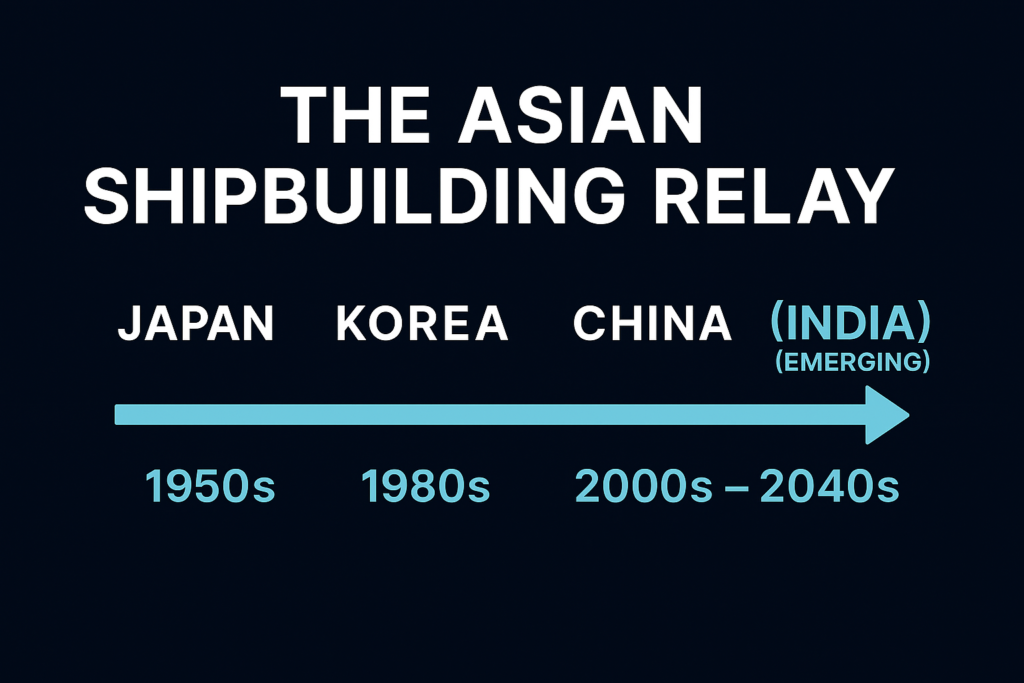

Japan → Korea → China formed a 50-year relay of capability building. India could become the fourth node — not a rival, but a collaborator.

1. Financing Synergy

China’s greatest maritime strength is not steel — it is finance. Chinese leasing companies and banks could co-finance Indian yard expansions, just as they already do in Southeast Asia.

2. Supply Chain Synergy

India lacks marine engines, LNG containment tech, and high-grade steel. China has all of these at scale.

Supplier migration is how Korea overtook Japan. India could follow the same path.

3. Market Synergy

China’s yards have been full for years. Overflow orders could move to India, with China supplying:

- blocks

- machinery

- design packages

- EPC support

This is how Vietnam and the Philippines grew.

4. Strategic Synergy

A stable India–China industrial corridor would:

- accelerate the green transition

- strengthen Asia’s maritime autonomy

- stabilise global supply chains

- create a multi-country innovation ecosystem

This is not a rivalry. This is co-evolution.

INDIA’S OPPORTUNITY: A NEW GENERATION OF SHIPYARDS

As India awakens to its maritime potential, a new generation of private shipyards will emerge — yards that:

- integrate global supply chains

- specialise in green-fuel vessels

- combine design, digitalisation, and environmental stewardship

- operate with private-sector agility

- build for coastal, inland, offshore wind, and regional trade

These yards will not replace China, Korea, or Japan. They will complement them.

India’s rise will strengthen the entire Asian maritime ecosystem.

CONCLUSION: A FUTURE BUILT ON COLLABORATION, NOT CONFRONTATION

India’s shipbuilding renaissance is not a threat. It is an invitation.

An Invitation to Build a More Balanced Asian Maritime Future.

An invitation to collaborate rather than compete.

An invitation to rediscover a legacy India once owned — and can own again.

A stronger India can make Asia stronger. A stronger Asia can make global shipping more resilient. And the next generation of Indian shipyards can help shape that future — not through rivalry, but through synergy.