Post 8/9 of the US–Korea Shipbuilding Series: Strategic alliances, nostalgia, and industrial revival—why Korea believes it can reboot U.S. shipbuilding, and why doubts remain.

Strategic alliances, nostalgia, and industrial revival—why Korea believes it can reboot U.S. shipbuilding, and why doubts remain.

A LEGACY FORGED IN STEEL

During World War II, American shipbuilding rose to a scale and speed the world had never seen. It was more than industry at work—it was a national symphony of purpose, where government, labour, and enterprise moved in perfect rhythm. Welders from the Deep South stood shoulder to shoulder with machinists from New England. Immigrants joined hands with Dust Bowl migrants. Women filled the yards in numbers once unimaginable. For a brief, extraordinary moment, racial, regional, and social divides blurred into a single, urgent mission: to build the ships that would decide the fate of the free world.

America didn’t just build ships—it built a miracle. Under the Emergency Shipbuilding Program, more than 6,000 vessels were launched between 1940 and 1945. Liberty Ships, the “Model T Fords of the ocean,” rolled off assembly lines in record time—some in just four days. Ships that carried troops and tanks across the Atlantic. Ships that in 1944 brought back shocked and starving German POWs from Europe’s collapsing fronts to the land of abundance—New York, Norfolk, and Boston. Entire shipyards sprang up from nothing, often led by companies with no prior shipbuilding experience. The mobilisation was so vast it absorbed billions in investment and employed armies of skilled workers.

This wasn’t simply production. It was choreography on a national scale—a fusion of engineering, logistics, and civic will. In those years, America became the world’s shipbuilding superpower.

But that was a different America. In the decades since, the nation has become entangled in a complex web of challenges. Today’s industrial landscape feels fragmented, weighed down by regulation, and often paralysed by political gridlock. The spirit of mobilisation that once astonished the world—the spirit that turned innovation into prolific output—has faded into inertia, buried beneath procedure and hesitation.

THE DECLINE OF U.S. SHIPBUILDING

The decline of U.S. shipbuilding after WWII was not caused by a single factor but by a convergence of neglect, policy missteps, foreign competition, and industrial erosion. America ignored the strategic importance of shipbuilding, lost momentum after wartime mobilisation, closed down commercial yards, shed its skilled workforce, and allowed foreign competitors to dominate with subsidies, scale, and innovation.

- Loss of Strategic Priority

- After WWII, shipbuilding was no longer treated as a national priority.

- Policymakers assumed America’s wartime dominance would endure, ignoring the need to sustain commercial yards.

- Unlike aviation or defence, shipbuilding slipped into the background, seen as an afterthought rather than a backbone industry.

- Momentum Lost

- The wartime miracle of building ships in four days was never institutionalised.

- Once the Emergency Shipbuilding Program ended, production collapsed.

- By the 1960s–70s, U.S. yards were already lagging behind Japan and Korea in efficiency and scale.

- Closure of Shipyards

- Instead of building on established infrastructure, hundreds of wartime yards were dismantled or converted to other industries.

- By 2023, China had 1,749 vessels under construction, while the U.S. had just five.

- America now builds less than 1% of global ships, leaving its coastline dependent on foreign-built vessels.

- Workforce Erosion

- Skilled welders, machinists, and naval architects drifted into other industries as demand collapsed.

- Today, the U.S. faces critical shortages of civilian mariners to crew Navy support vessels.

- Workforce gaps mean even funded naval programs are delayed by years.

- Policy Constraints

- The Jones Act created a captive domestic market, deterring innovation and scale.

- U.S. yards were shielded from competition but also starved of global demand.

- Meanwhile, foreign governments poured subsidies into their shipyards, creating global champions.

- Infrastructure Decay

- The U.S. yards that survived the post-war contraction failed to modernise with automation, modular construction, and digital design.

- Facilities grew outdated, unable to compete with the sprawling, high-tech complexes rising in South Korea and China.

- Today, even flagship naval programs—such as the Ford‑class carriers and Virginia‑class submarines—are years behind schedule and burdened by staggering cost overruns.

- Supply Chain Fragmentation

America lost control of its maritime supply chain:

- 95% of shipping containers are built in China.

- 80% of U.S. port cranes come from a single Chinese company.

This dependence further undermines domestic shipbuilding capacity.

Summary

The decline of U.S. shipbuilding is a story of lost momentum, policy neglect, workforce erosion, and industrial decay. While America once built miracles, today it builds less than 1% of global ships, with naval programs plagued by delays and cost overruns. Meanwhile, China, Korea, and Japan dominate the industry, leaving America strategically vulnerable.

THE RISE OF THE EAST — AND THE AWAKENING OF THE WEST

For decades, the Far East quietly reshaped the maritime world. Japan learnt ‘block’ construction methods from the US and perfected them with precision. Korea scaled global partnerships, and China—backed by state ambition—built not only the world’s largest commercial fleet but also a formidable navy. The pace and scale of China’s naval expansion have jolted Washington from its post-Cold War slumber.

The U.S. now faces a strategic imperative: to build ships not just better, but faster and in far greater numbers. Yet this is not the America of WWII—industrial muscle has thinned, shipyards have vanished, and the urgency of national defence must now contend with fragmented supply chains and regulatory inertia. The question is no longer whether America can revive shipbuilding, but whether it must—and how quickly.

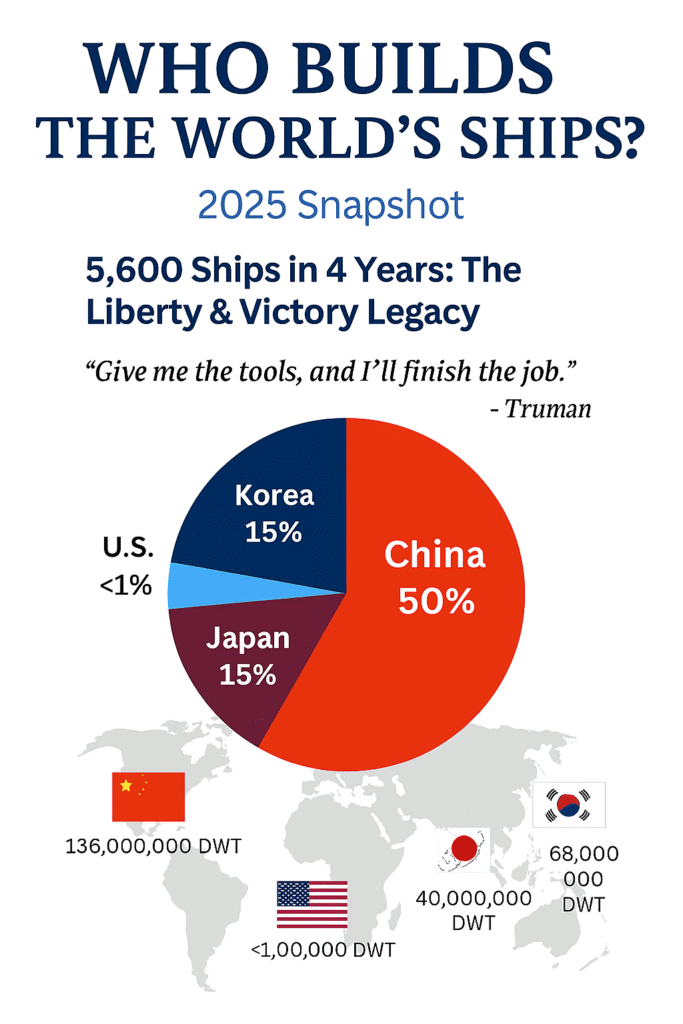

GLOBAL SHIPBUILDING LANDSCAPE (2025 SNAPSHOT)

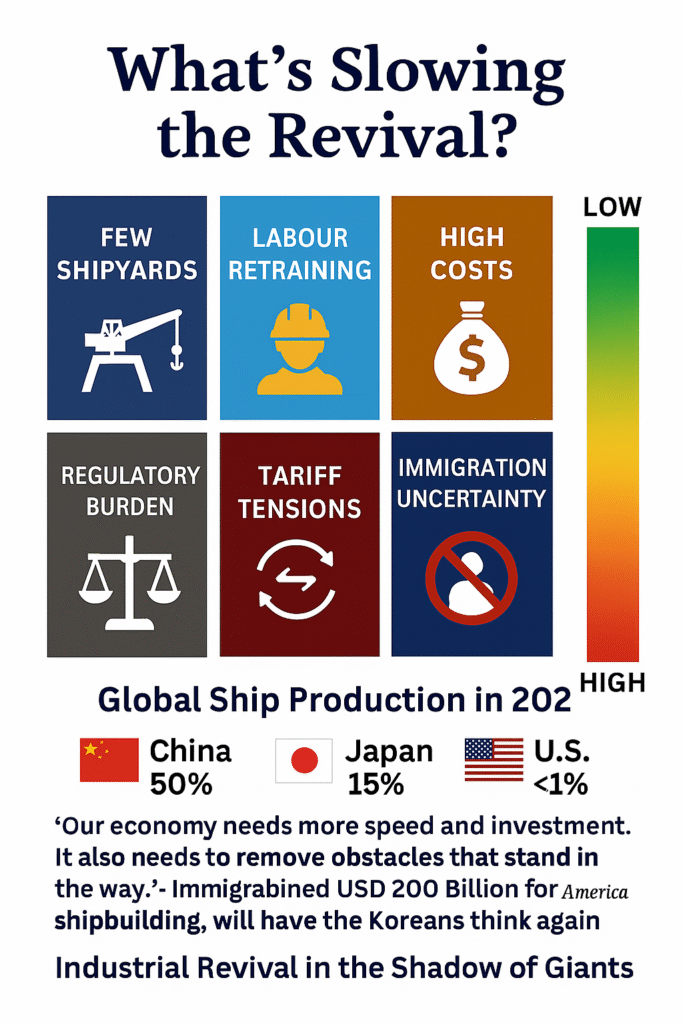

Global shipbuilding today is dominated by Far Eastern yards—China, South Korea, and Japan. China leads in total tonnage, while Korea commands the high-value segment with LNG carriers, FLNGs, and FPSOs. America, by contrast, builds less than 1% of the world’s ships.

Even the Navy’s own programs are years behind schedule, weighed down by cost overruns and supply chain bottlenecks. China, meanwhile, has surged ahead: by 2024, it achieved 200 times more shipbuilding capacity than the U.S., and continues to grow. With its strategic interests stretching across every ocean, this is a Rip Van Winkle wake-up call for America.

WHY SHIPBUILDING IS THE BACKBONE OF A NATION

Shipbuilding is power.

Shipbuilding is independence.

Shipbuilding is destiny.

The United States stands at a crossroads. A nation that builds ships commands the seas, controls its trade, and secures its defence. A nation that neglects shipbuilding risks dependence on foreign yards, surrendering both freedom and strength. Once the infrastructure dies, the skills die with it—and rebuilding is slow, painful, sometimes impossible.

America cannot afford that loss. America cannot afford that silence. America cannot afford that surrender.

America must build. America must build now. America must build fast. Not a handful of vessels, not a token fleet, but ships in numbers, ships in scale, ships in speed. China can launch more ships in a month than America can in a year. That is not just technology—it is tempo. And tempo wins wars. Tempo wins oceans. Tempo wins the future.

The nation that builds faster will rule the seas. The country that rules the waters will rule tomorrow. And tomorrow belongs to those who build today.

COMMERCIAL YARDS AS FOUNDATION

Sustainable naval shipbuilding depends on thriving commercial yards.

- A nation cannot rely solely on naval yards for wartime surges.

- Even technically competent naval yards cannot deliver the sheer volume and speed of platforms required in a conflict.

- Only commercially successful shipyards, geared to building merchant fleets at scale, can pivot quickly to naval production when needed.

- This was the WWII model: Liberty Ships and naval vessels rolled out side by side, with commercial yards seamlessly switching to defence needs.

Jobs and Workforce

Shipbuilding is a jobs engine:

- In the U.S., 105,652 direct jobs in shipbuilding and repair.

- Each job supports 2.6 more in the supply chain, from steel mills to electronics, logistics, and advanced manufacturing.

- Total impact: ~400,000 jobs across all 435 Congressional districts.

- Historically, WWII shipbuilding employed 1.4 million workers, proving its capacity to absorb and mobilise manpower at scale.

Technology and Innovation

Shipbuilding drives technological advancement:

- Welding, metallurgy, propulsion, and digital design innovations spill into aerospace, automotive, and energy sectors.

- Modern shipyards are hubs for green technologies (LNG, hydrogen, ammonia fuels) and digital twin engineering.

- These advances ripple outward, strengthening national industrial competitiveness.

Multiplier Effect

The economic multiplier is significant:

- Every shipyard job generates 2.6 additional jobs in related industries.

- Shipbuilding contributes $42.4 billion in GDP annually in the U.S.

- In Europe, shipbuilding and repair employ 316,000 people and generate €19.9 billion in GVA, showing similar multiplier effects.

- This makes shipbuilding one of the most strategically valuable industries for both defence and economic policy.

Why This Matters For America

The stakes extend far beyond America’s shores. Oceans are the arteries of global commerce, carrying the lifeblood of economies everywhere. If America falters in shipbuilding, the balance of maritime power shifts—and with it, the security of trade routes, the freedom of navigation, and the stability of international markets. The race to build ships is not only America’s challenge; it is a contest that will shape the future of global order. The world has a vested interest in whether America can rise to meet it.

- Without commercial shipbuilding success, naval shipbuilding cannot scale in emergencies.

- Shipbuilding is not just about ships—it is about jobs, technology, and industrial resilience.

- The multiplier effect ensures that investment in shipyards strengthens entire ecosystems of ancillary industries, from steel to electronics.

- Reviving U.S. shipbuilding is therefore not optional; it is a national imperative for both economic vitality and defence readiness.

AMERICA HAS THE INGREDIENTS

The United States not only possesses every ingredient needed to reignite its shipbuilding industry, but it is also, in fact, tempting on the surface:

- Leadership resolve—a renewed eagerness to restore America’s shipbuilding greatness.

- Abundant raw materials—steel, copper, and nickel, the essential backbone of modern ship construction.

- Expansive coastline—19,924 miles across the Atlantic and Pacific, surpassing China and South Korea combined, offering unmatched maritime access.

- Capital—abundant and mobilised. JPMorgan’s $1.5 trillion Security and Resiliency Initiative—including shipbuilding—signals that Wall Street is no longer watching from the sidelines. Korea pledged up to $200 billion in U.S. shipbuilding, beginning with Hanwha’s $5 billion injection into the Philadelphia shipyard, coupled with training and shared expertise from their world-class facilities.

- Manpower potential—a large population, easily trainable, which could be mobilised into a skilled shipbuilding workforce.

- Academic excellence—the world’s leading marine universities and research institutions are in the U.S., driving pedagogy, innovation, and R&D.

- Global alignment—adherence to international standards that ensure competitiveness and credibility worldwide.

On paper, America has everything it needs to lead the world in shipbuilding once again. And yet, there is a sobering parallel. America also has every reason—and every ingredient—to build a network of bullet trains. The raw materials, the capital, the coastline, the technology, the manpower, the academic excellence—all are present. But the trains were never built. The vision was never mobilised. The mindset faltered.

This raises the uncomfortable question: will shipbuilding suffer the same fate? Will America, despite having all the ingredients, fail to mix them into a recipe for revival? The answer lies not in resources, but in resolve.

STRUCTURAL HEADWINDS

Despite its strengths, America faces deep-rooted challenges:

- Shipyard Scarcity: Commercial operational yards are too few to scale production. Greenfield shipyards surrounded by a manufacturing base that supports the effort must be built—an expensive, time-consuming endeavour.

- Workforce Readiness: Retraining civilians for industrial shipbuilding in today’s digital era is no small feat. Unlike WWII, motivation is harder to summon in peacetime.

- Cost Competitiveness: U.S. labour costs, regulatory compliance, and fragmented supply chains make shipbuilding significantly more expensive than in China or Korea.

- Tariff Tensions: Rising trade friction—heavy tariffs on ships built in the U.S. visiting China and vice versa—creates uncertainty and commercial risk. Chinese sanctions against US-linked Hanwa units are seen as a warning gesture aimed at Philly shipyard, although it has no immediate threat; these could escalate in the future.

- Policy Volatility: Long-term industrial investment demands policy stability. America’s political cycles often disrupt continuity, deterring strategic capital.

- Geopolitical Labour Risk: One of the main triggers of the American shipbuilding revolution during WWII was imported labour. Today, however, uncertainty triggered by President Trump’s new policy on foreign workers—including ICE raids and deportations of Korean workers—casts a shadow over Korea’s $200 billion investment pledge. Korean shipbuilders may reconsider their U.S. commitments amid rising immigration enforcement and diplomatic strain.

- Endless Redesign Amid Construction: Leading to rework, delays, over-budget, abandoned projects and billions wasted.

THE CULTURAL BARRIER — WHEN MANPOWER ISN’T ENOUGH

America has a large population. It has the training infrastructure. It has the capital. On paper, the manpower potential is vast. But the trend may prove otherwise.

In Japan, shipyard jobs are increasingly shunned by the younger generation, who prefer “clean jobs” in banking, tech, and office environments. Shipbuilding is seen as part of the “3K” category—kitanai (dirty), kitsui (hard), and kiken (dangerous). Despite Japan’s maritime legacy, the youth drift toward prestige, comfort, and digital careers.

The same drift is visible in the United States. Young Americans gravitate toward remote work, creative industries, and tech-enabled roles. Shipyard jobs—sweaty, noisy, physically demanding—are often perceived as relics of a bygone era. Even with high pay and job security, these roles struggle to attract Gen Z workers.

This is the paradox: while America has the numbers to train a new shipbuilding workforce, the cultural appetite may be missing. The digital era has reshaped career aspirations. Without a shift in perception, shipbuilding risks becoming another industry with jobs available but no takers.

To overcome this, shipbuilding must be reframed—not as “dirty work,” but as nation-building work. It must be branded as high-tech, purpose-driven, and patriotic. The industry must speak to the values of the next generation: innovation, impact, and identity.

Otherwise, even with foreign investment and infrastructure, the revival may stall—not for lack of resources, but for lack of resonance.

REBRANDING SHIPBUILDING — FROM SWEAT TO STRATEGY

If America is to revive shipbuilding, it must not only build yards and legislate manpower—it must rebrand the industry itself. For too long, shipyard jobs have been seen as “dirty, sweaty, and outdated.” In the digital era, that perception is fatal. To attract the next generation, shipbuilding must be reframed as nation-building work: high‑tech, purposeful, and globally competitive.

1. PATRIOTISM AND PURPOSE

- Position shipbuilding as a national mission, akin to space exploration or defence.

- Campaigns should highlight the role of shipbuilders in securing America’s freedom, trade, and global leadership.

- Narratives must shift from “dirty work” to heroic work—the hands that build ships are the hands that safeguard the nation.

2. TECHNOLOGY AND INNOVATION

- Showcase shipyards as digital factories: automation, robotics, AI-driven design, and green propulsion systems.

- Present welding and fitting not as manual drudgery, but as precision engineering supported by cutting-edge tools.

- Link shipbuilding to climate solutions: LNG, hydrogen, and ammonia fuels—making it part of the clean‑energy future.

3. CAREER PRESTIGE AND PATHWAYS

- Create clear vocational pipelines from high schools, community colleges, and universities into shipbuilding careers.

- Offer apprenticeships that combine hands-on skills with digital training, making shipbuilding a hybrid of craft and tech.

- Elevate shipbuilding jobs to the same prestige as coding or finance—emphasising pay, security, and impact.

4. GLOBAL COLLABORATION

- Highlight partnerships with Korea and Japan as opportunities for American youth to learn world-class methods.

- Position shipbuilding as a global career: skills gained in U.S. yards are transferable to projects worldwide.

- Encourage exchange programs and joint training to make shipbuilding aspirational, not provincial.

5. CULTURAL CAMPAIGNS

Launch national campaigns that celebrate shipbuilders as innovators and patriots.

- Use storytelling—documentaries, social media, even cinematic narratives—to reframe the image of the shipyard.

- Just as Silicon Valley became a cultural symbol of innovation, shipyards must become symbols of resilience and pride.

THE CORE MESSAGE

Shipbuilding must be sold not as sweat, but as strategy. Not as “dirty work,” but as nation-building work. If America can rebrand the industry to resonate with the values of Gen Z—innovation, purpose, and global identity—then the manpower challenge can be overcome.

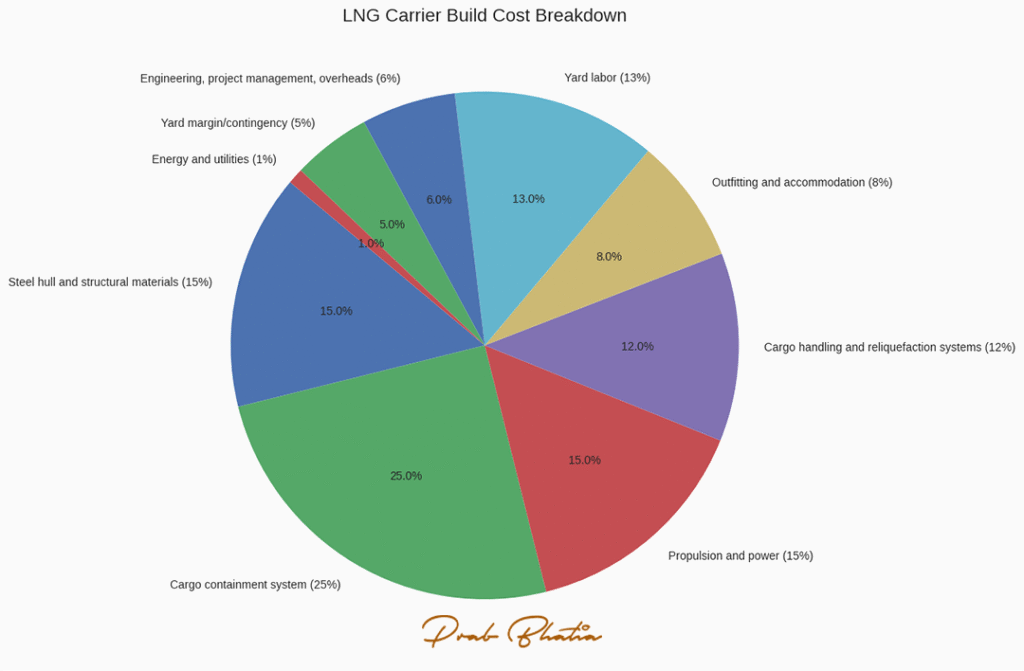

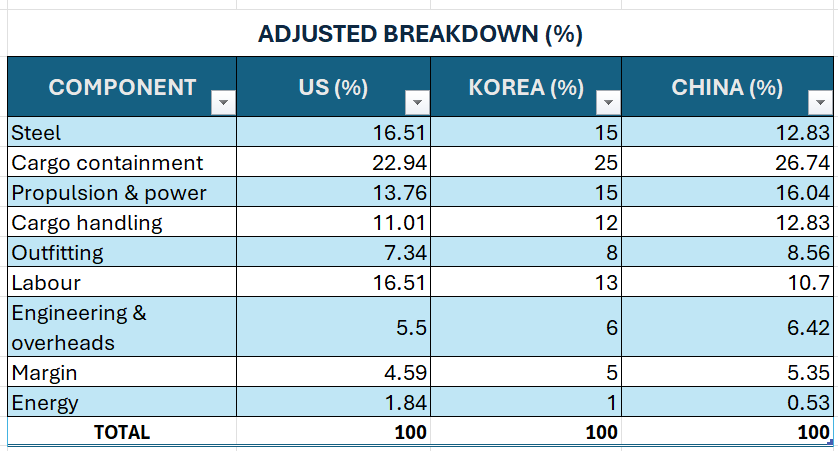

COST MODEL OF AN LNG CARRIER (174,000 M³) BY COUNTRY

The chart below illustrates the percentage of main components that contribute to the total cost of building an LNG carrier in Korea:

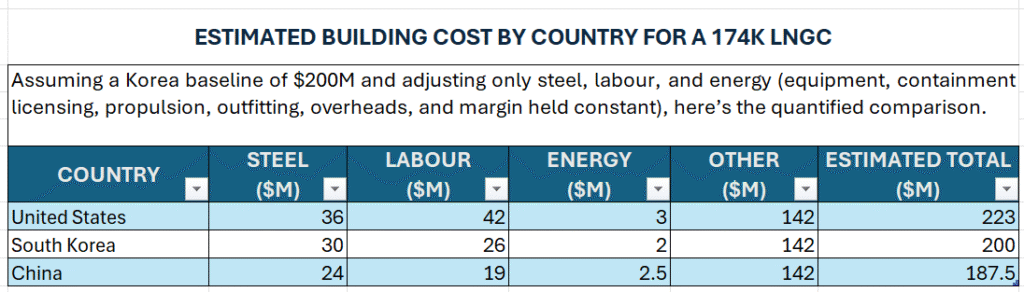

After adjusting average cost differences in steel, labour, and energy across the United States, South Korea, and China, the relative cost of building a 174K LNG carrier in the US, South Korea and China is illustrated the table below:

From these estimates, it can be seen that the major cost differences between the three countries arise from steel, labour, and, to a lesser extent, energy prices. With South Korea as the baseline at $200M, and adjusting only steel, labour, and energy (while holding equipment, containment licensing, propulsion, outfitting, overheads and margins remaining constant), the relative total cost of building the LNG carrier in the US, Korea and China is shown below:

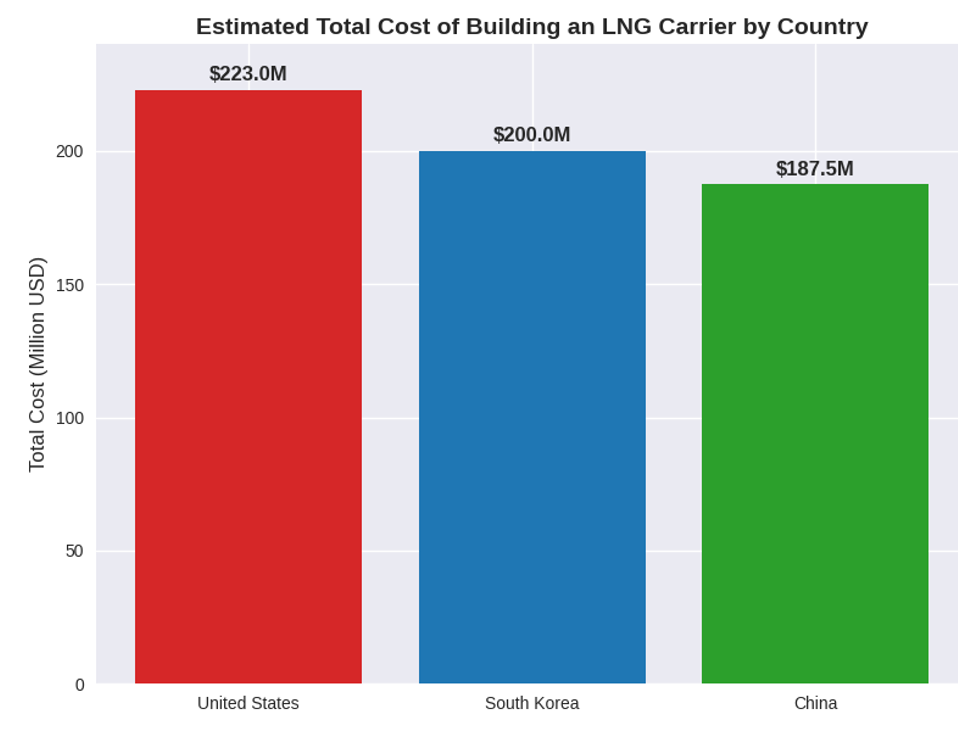

Thus, for a 174,000 m³ LNG carrier, the estimated build costs are:

- United States: ~$223M—highest cost due to expensive steel and labour.

- South Korea: ~$200M—balanced productivity and costs, making it the global leader.

- China: ~$187.5M—lowest cost thanks to cheaper steel and labour, though productivity remains lower.

QUICK TAKEAWAYS

Equipment/heavy components: Cargo containment and propulsion are globally sourced and technology-driven, so their shares remain relatively stable across countries.

- United States: Significantly higher labour and steel inflate the cost structure; energy remains a minor contributor (<2%), adding only a minor bump.

- South Korea: Balanced costs and high productivity explain its dominance in LNG carrier construction.

- China: Lower steel and labour compress total costs, but containment and propulsion take relatively larger shares after normalisation. Although China benefits from lower wages, its productivity lags.

CONTEXTUAL NOTE

These illustrations represent a typical LNG carrier of 174,000 m³. Actual costs vary depending on design complexity, containment system choice, and propulsion technology. In practice, shipowners often prefer South Korea, where efficiency, advanced production methods, and proven expertise ensure reliable delivery. China is increasingly attractive for its lower upfront costs, supported by cheaper steel and labour, though productivity and quality standards are still catching up.

By contrast, the United States remains structurally uncompetitive. Higher labour and steel costs, combined with limited LNG shipbuilding experience, make domestic construction significantly more expensive and less efficient.

THE GULF/SINGAPORE MODEL — LESSONS IN MANPOWER

Shipbuilding is not just steel and docks; it is people. Without skilled hands, even the most advanced yard is nothing more than empty infrastructure. Singapore understood this early. Its competitive ship repair and conversion industry generates billions annually, sustained by a steady inflow of skilled contract workers from Asia. Welders, fitters, and machinists from India, Bangladesh, and the Philippines keep the yards humming, ensuring Singapore remains a global hub for maritime services.

The Gulf countries, too, thrive on imported manpower. The UAE’s shipyards and drydocks are built on the shoulders of contract workers, whose skills and discipline underpin the region’s maritime success. Even advanced shipbuilding nations like Korea and Japan have begun importing skilled labour from India, the Philippines, and Vietnam to offset domestic shortages. Korea, for instance, has expanded foreign worker quotas in shipyards by more than 30% in recent years, acknowledging that without manpower, industrial ambition stalls.

This raises a hard truth for America. If new shipyards are commissioned, the growing skill shortage will quickly become the bottleneck. Domestic training programs can help, but they take years to mature. In the short term, the only proven model is the one Singapore, the Gulf, Korea, and Japan already use: importing skilled contract workers to fill the gap and keep the cost down.

To succeed, U.S. shipbuilding must embrace the reality that manpower is global. Just as steel and equipment are imported to compete internationally, so too can skill—at least until domestic training programs catch up. Shipbuilding is, by its very nature, an international business. Nations that thrive in this industry do so by competing globally, not by walling themselves off. One cannot hope to play on the world stage while clinging to restrictive policies and the same costly, outdated labour models that helped destroy America’s and Europe’s shipbuilding in the first place. If the U.S. is serious about revival, it must recognise that manpower, like materials, is part of the global supply chain — and legislate accordingly.

Shipyards without workers are empty docks. If America is serious about reviving shipbuilding, it must not only build infrastructure but also legislate for the workforce that will bring those yards to life.

EXECUTIVE SUMMARY

South Korea continues to lead global LNG carrier construction, combining efficiency and proven expertise to deliver competitive costs. China leverages cheaper steel and labour to lower upfront prices, though productivity still trails Korea. The United States, burdened by higher labour and steel costs and lacking LNG shipbuilding experience, remains structurally uncompetitive in this segment.

Yet as one of the world’s leading LNG exporters, the U.S. faces a strategic imperative: it must develop commercial shipbuilding capacity, especially for LNG carriers, to deliver its gas reliably worldwide. This challenge is magnified by global demand trends: Qatar’s Energy Minister Al-Kaabi projects LNG demand will surge from 400 million to 700 million tons annually within the next decade, driven by insufficient infrastructure investment and the AI-fuelled energy boom.

But infrastructure alone is not enough. As the Singapore and Gulf models show, shipbuilding is sustained by globally sourced skilled labour. Even Korea and Japan now rely on imported workers to remain competitive. Without a global manpower strategy, the U.S. cannot hope to compete internationally. Shipyards without workers are empty docks; America must legislate not only for steel and infrastructure, but also for the workforce that will bring those yards to life.

CAN KOREA REALLY MAKE AMERICA’S SHIPBUILDING GREAT AGAIN?

South Korea has emerged as the world’s most sophisticated builder of high-value vessels—LNG carriers, FLNGs, FPSOs—platforms that demand precision engineering and modular construction at scale. Korean yards like Hyundai, Samsung, and Hanwha have mastered the art of building complex ships faster and more efficiently than anyone else. It is this expertise that Washington now hopes to import.

Under ambitious new agreements, Korea has pledged billions to modernise U.S. yards, train American workers, and transfer technology. The idea is simple: if America cannot rebuild shipbuilding muscle alone, perhaps Korea can help graft its methods onto U.S. soil. Joint ventures, workforce exchanges, and co-production programs are being touted as the path to revival. Japan, too, has joined this effort, pledging capital and expertise to strengthen America’s maritime base.

Yet not everyone is convinced. There is a paradox at the heart of the Korean/Japanese adventure in the States. On one hand, the investments are vast, the intentions serious, and the need undeniable. On the other hand, America’s industrial inertia, regulatory gridlock, and manpower shortages may prove too entrenched for foreign capital alone to overcome. Without a national will to mobilise—the kind last seen in WWII—even the best Korean technology may find itself stranded in empty American docks.

The question, then, is not whether Korea can make America’s shipbuilding great again, but whether America itself is ready to embrace the scale, speed, and global mindset required. Korea can provide the tools, the training, and the know-how. But only America can supply the urgency.

CONCLUSION

America once astonished the world with its shipbuilding miracle. Today, Korea and Japan stand ready to graft their expertise onto U.S. soil. But foreign capital and technology alone cannot substitute for national will. America must decide whether it will mobilise — or whether shipbuilding will join bullet trains as another unrealised ambition.

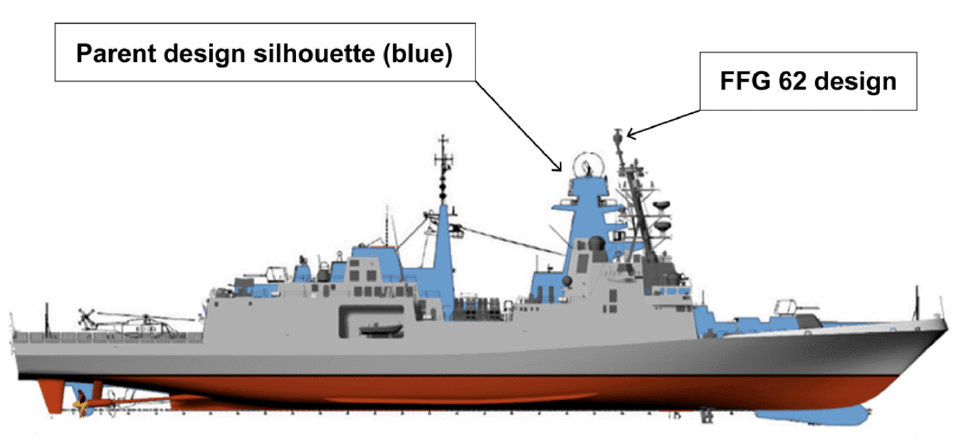

The recent termination of four ships from the troubled Constellation-class guided missile frigate program underscores the systemic faults crippling U.S. naval shipbuilding. Based on an imported Italian design from Fincantieri Marinette Marine rather than an indigenous one — despite America’s immense knowledge base — the program has already suffered a 36-month delay. Only the first two frigates are expected to be completed in April 2029. Once again, design work lagged behind fabrication, forcing costly rework, delays, and budget overruns. The Navy must confront its hierarchical flaws and, above all, stop cutting steel before the design is finalised — and then stick to it.

This is not simply a technical failure — it is a philosophical one. Naval shipbuilding has become trapped in the pursuit of a Platonic ideal: the perfect warship that exists only in theory. Likewise, it has been seduced by a utopian vision of flawless vessels, imagined but unattainable in practice. The result is paralysis: ships endlessly revised mid-construction, projects abandoned, and billions wasted.

Engineering must recognise that perfection belongs to philosophy, not to the shipyard. The lesson from WWII shipbuilding, from Korean and Japanese commercial yards, and even from industries like automobiles and smartphones is clear: finalise the design, build it within time and budget, and roll improvements into the next generation. Each vessel should be seen as a step forward, not the unattainable end state.

“Stop chasing utopias — start building ships.”

If the U.S. Navy continues to chase Platonic or utopian perfection during construction, it will keep producing delays and overruns instead of ships. To restore credibility and efficiency, shipbuilding must embrace discipline: freeze designs, enforce time and budget limits, and accept that iteration — not endless revision — is the true path to progress.

It must also be remembered that for naval shipbuilding to succeed meaningfully, America must rebuild a competent commercial shipbuilding base to compete with South Korea and China. That is possible, but not without the same concerted effort and national will that once drove the manufacturing revolution during WWII. Given the impediments in the system today, that may remain a distant dream. As one seasoned voice from Exxon observed: “As for the Korean‑US ambitious plans to revive U.S. shipbuilding, it is good money thrown after a bad project. Short of, God forbid, an all‑out war, I do not see a significant rise in U.S. commercial shipbuilding in the next 20 years, if ever.”

That scepticism is real. But so too is the possibility. America has the ingredients. Korea can provide the spark. The question is whether America will supply the flame.

“Steel waits for the hand that dares — ships are built not by ingredients alone, but by resolve.”

Another great shipbuilding narrative by Mr Bhatia. Sums up macro facts with a dose of reality. Must read!

Thank you, Anil. Glad the narrative struck a chord, especially coming from someone who’s seen the tides shift firsthand, your words mean a lot!

Great writing.

Thank you, Rajan. Your support means a lot.

US commercial shipbuilding holds a merly less than 1 % of global tonnage, down from historical leadership, due to high labor costs, skilled proffessional shortages, regulatory red tape and outdated methods that make ships costlier and slower to build , China’s capacity dwarfs America’s by over 230 times in naval terms, with its navy projected at 435 ships by 2030 versus the US’s 239. New US tariffs and port fees on foreign vessels add costs but highlights reliance on imports . Partnerships with South Korea, which built 3,000 ships in a decade and eyes US collaborations like icebreakers and repairs, offer a pragmatic path to rebuild capacity without full domestic revival . Decarbonization pressures, including IMO net-zero goals by 2050, will demand fleet renewal which may find US limping in the end.

Guru, I fully agree with your sharp assessment of where U.S. shipbuilding stands today. The gap with China is indeed a ravine, but I believe it can be narrowed if America takes corrective measures—serious investment, leaner practices, and technical know‑how from Korea and Japan. Korea’s record of thousands of ships in a decade shows what disciplined ecosystems can achieve, and Japan’s engineering precision is another reservoir to draw from.

Equally, the intellectual pipeline needs fixing. Too many of the brightest youth chase management, medicine, law, or banking, while engineering struggles to attract top talent. Unless engineering is re‑framed as a national calling, America will limp into the decarbonization era. Fleet renewal under IMO’s net‑zero goals will demand not just ships, but minds. If the U.S. can align its youth, its policies, and its partnerships, revival is possible within a decade.

You are correct and your insights resonate deeply with the challenges and opportunities ahead for U.S. shipbuilding. The comparison with Korea’s disciplined shipyards and Japan’s engineering prowess truly highlights what focused ecosystems and technical excellence can accomplish. I completely agree that reclaiming leadership will require not just investment, but a cultural shift—valuing engineering as a vital national mission to attract the brightest minds. As you rightly point out, aligning education, industrial policy, and international collaboration can create a powerful synergy. The coming decarbonization push under IMO’s net-zero mandate indeed demands innovative ship design and engineering solutions. If the U.S. leverages its strengths wisely, it can bridge that gap and lead a sustainable maritime future within the next decade. Your call to action is both timely and inspiring. On a personal note you are not only excellent photographer but you have very deep and thorough knowlege of international shipping , proud of you.

Guru, your words truly humble me. Coming from a seasoned maritime professional like yourself, your appreciation carries special weight. I deeply value your encouragement and the wisdom reminds me how much our industry owes to voices like yours. Please keep sharing your thoughts in the future too.